Student Loan Interest Deduction: Maximize Your Tax Savings

Student loan debt can feel like a never-ending burden, looming over your financial future. But did you know there's a way to potentially lighten that load, at least a little, when tax season rolls around? Let's explore the student loan interest deduction and how you can use it to your advantage.

For many, navigating the complexities of tax deductions can feel like wading through a confusing maze. Figuring out what you're eligible for, gathering the necessary documents, and understanding the limits can be time-consuming and frustrating. The fear of making a mistake and potentially facing penalties only adds to the stress.

This article aims to guide you through the ins and outs of the student loan interest deduction. We'll break down the eligibility requirements, explain how to calculate the deduction, and highlight key considerations to help you maximize your tax savings. By understanding this deduction, you can potentially lower your tax bill and free up some extra cash.

Ultimately, understanding and utilizing the student loan interest deduction can provide some much-needed financial relief. We'll explore eligibility, deduction limits, and strategies to maximize your savings, helping you navigate the complexities of this valuable tax benefit. The key words are student loan interest deduction, tax savings, eligibility, deduction limits, and tax benefit.

Personal Experience with Student Loan Interest Deduction

I remember the first time I filed taxes after graduating college. Buried under a mountain of forms and confusing jargon, I felt completely lost. The sheer volume of my student loan debt loomed large, and the thought of figuring out taxes on top of everything else was overwhelming. A friend mentioned the student loan interest deduction, and I initially dismissed it as too complicated. However, after a bit of research, I discovered it was actually quite straightforward and could potentially save me some money. I meticulously gathered my 1098-E form, carefully calculated my deduction, and nervously submitted my return. To my relief, the deduction was accepted, and I received a slightly larger refund than expected. That small victory provided a much-needed boost and instilled a newfound confidence in my ability to manage my finances. It was a valuable lesson in the importance of exploring all available tax benefits, no matter how daunting they may seem initially. The student loan interest deduction helps ease burden, lower tax bill and minimize confusion.

What is the Student Loan Interest Deduction?

The student loan interest deduction allows you to deduct the interest you paid on qualified student loans during the tax year. It's an above-the-line deduction, meaning you can claim it even if you don't itemize your deductions. This is a significant advantage for many taxpayers, as it simplifies the process and makes the deduction more accessible. The maximum deduction amount is currently $2,500, and it's subject to income limitations. The loan must have been taken out for yourself, your spouse, or a dependent. It’s crucial to understand that the loan proceeds must have been used for qualified education expenses, such as tuition, fees, room and board, and books. Refinanced student loans are also eligible, provided they meet the original requirements. Understanding these criteria is the first step in determining your eligibility and maximizing your potential tax savings. It's a tool for repayment and tax reduction. For many taxpayers, a deduction is an advantage to simplify the tax process. The eligibility and the criteria, determine the tax savings.

History and Myths of Student Loan Interest Deduction

The student loan interest deduction has been around for a while, evolving over the years in response to the increasing burden of student loan debt. Initially, it was introduced to provide some tax relief to borrowers struggling to repay their loans. Over time, the deduction limits and eligibility requirements have been adjusted to reflect changing economic conditions and policy priorities. One common myth is that the student loan interest deduction is only for recent graduates. While it's true that many recent graduates benefit from it, the deduction is available to anyone who meets the eligibility requirements, regardless of their age or how long they've been out of school. Another myth is that you can deduct the entire amount of interest you paid. While the maximum deduction is $2,500, your actual deduction may be limited based on your income and other factors. Understanding the history and dispelling these myths is essential for accurately assessing your eligibility and maximizing your potential savings. It encourages policy priorities and tax relief to anyone with student loan and meets the eligibility requirements.

Hidden Secrets of Student Loan Interest Deduction

One often overlooked aspect of the student loan interest deduction is the impact of loan consolidation and refinancing. While consolidating or refinancing your student loans can simplify your repayment and potentially lower your interest rate, it's crucial to ensure that the new loan qualifies for the deduction. Generally, as long as the new loan meets the original requirements – meaning it was used for qualified education expenses – it will be eligible. Another hidden secret is the interaction between the student loan interest deduction and other tax benefits, such as the tuition and fees deduction or the American Opportunity Tax Credit. In some cases, claiming one benefit may limit your ability to claim another. It's important to carefully analyze your situation and determine which combination of benefits will result in the greatest tax savings. Consulting with a tax professional can be invaluable in navigating these complex scenarios. It can affect your loan repayment and may reduce your tax benefits.

Recommendation of Student Loan Interest Deduction

My top recommendation for anyone with student loans is to carefully review your tax situation and determine if you're eligible for the student loan interest deduction. Start by gathering your 1098-E form from your loan servicer, which will show the amount of interest you paid during the year. Next, assess your income and determine if you meet the income limitations. If you're unsure, consult with a tax professional or use tax preparation software to help you calculate your deduction. Don't leave money on the table! Even a small deduction can make a difference in your overall tax liability. Finally, remember to keep accurate records of all your student loan payments and related expenses, in case you need to substantiate your deduction in the future. Claiming the tax break helps in your tax liability and remember to keep all of your records.

Maximizing Your Student Loan Interest Deduction

To maximize your student loan interest deduction, consider these strategies. First, make sure you're claiming the full amount of interest you paid, up to the $2,500 limit. If your income is close to the limit, explore ways to reduce your adjusted gross income (AGI), such as contributing to a traditional IRA or HSA. These contributions can lower your AGI and potentially make you eligible for a larger deduction. Additionally, be mindful of the timing of your student loan payments. If possible, try to make extra payments before the end of the year to increase the amount of interest you pay and potentially boost your deduction. However, always prioritize your overall financial well-being and ensure that making extra payments aligns with your budget and financial goals. Always consider your deduction limit and consult a financial advisor for other options. Don't forget to be mindful of the timing of your payments.

Student Loan Interest Deduction Tips

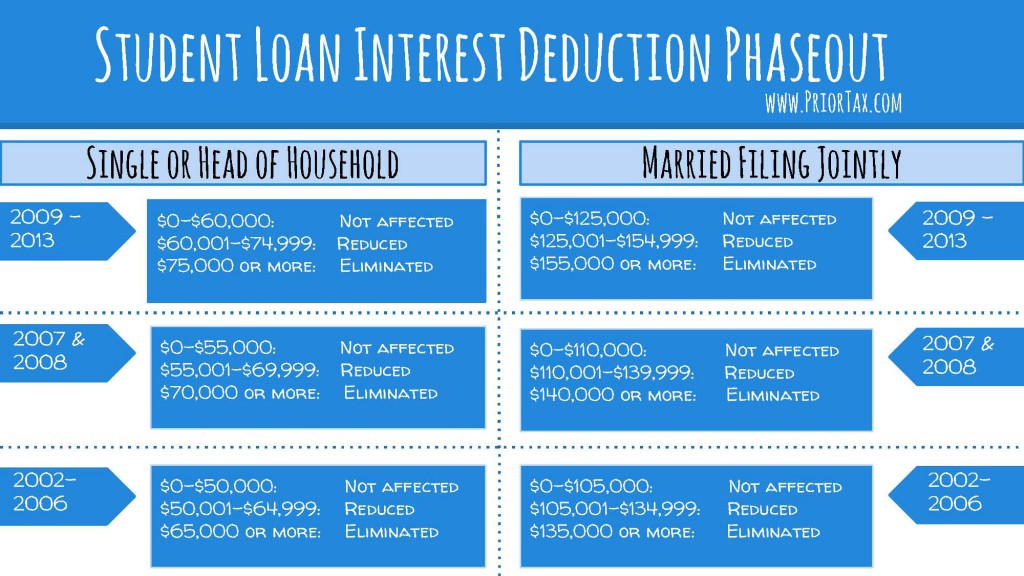

Here are a few extra tips to keep in mind when claiming the student loan interest deduction. Be aware of the phase-out ranges for the deduction, which vary depending on your filing status. For example, the deduction may be reduced or eliminated if your modified adjusted gross income (MAGI) exceeds a certain threshold. Also, remember that you can only deduct interest that you actually paid during the tax year. If you made any payments that were applied to principal, you can't deduct that portion. Finally, keep in mind that the student loan interest deduction is not the same as student loan forgiveness. While the deduction can provide some tax relief, it doesn't eliminate your student loan debt. Be aware of the deduction phase-out and keep in mind that the student loan interest deduction is not the same as student loan forgiveness.

Avoiding Common Mistakes

One of the most common mistakes people make when claiming the student loan interest deduction is failing to accurately calculate their deduction. Be sure to carefully review your 1098-E form and double-check your calculations. Another mistake is claiming the deduction when you're not eligible. Before claiming the deduction, make sure you meet all the eligibility requirements, including the income limitations and the qualified loan criteria. Finally, be sure to keep accurate records of all your student loan payments and related expenses. In case you're audited by the IRS, you'll need to provide documentation to support your deduction. Be sure to review your 1098-E form and document your student loan payments.

Fun Facts of Student Loan Interest Deduction

Did you know that the student loan interest deduction is one of the most commonly claimed tax deductions? Millions of taxpayers take advantage of this benefit each year. Another interesting fact is that the deduction is available even if you're not currently making payments on your student loans. If your loans are in deferment or forbearance, you can still deduct the interest that accrued during that period. Also, keep in mind that the student loan interest deduction is a federal tax deduction. Some states also offer their own student loan interest deductions, so be sure to check your state's tax laws as well. There are millions of tax payers take advantage of tax benefit each year, and may be available when you are not currently making payments.

How to Claim Student Loan Interest Deduction

Claiming the student loan interest deduction is relatively straightforward. You'll need to file Form 1040 and include the deduction on line 33, where it's specifically designated for student loan interest. You'll need your 1098-E form to report the amount of interest you paid. Tax preparation software can guide you through the process and automatically calculate your deduction based on your income and other factors. If you're filing your taxes manually, be sure to carefully follow the instructions on Form 1040. Remember to keep a copy of your tax return and all supporting documentation for your records. Use Form 1040 to report the amount of interest you paid and remember to keep a copy of your tax return.

What If You Don't Qualify for the Student Loan Interest Deduction?

If your income is too high to qualify for the student loan interest deduction, there are still other options for managing your student loan debt. Consider exploring income-driven repayment plans, which can lower your monthly payments based on your income and family size. You may also be eligible for student loan forgiveness programs, depending on your profession and loan type. For example, teachers, nurses, and other public service employees may qualify for Public Service Loan Forgiveness (PSLF). Explore alternative repayment plans or potential student loan forgiveness programs. These options can provide relief and help you manage your debt.

Listicle of Student Loan Interest Deduction

Here's a quick list of key things to know about the student loan interest deduction:

- It's an above-the-line deduction, meaning you can claim it even if you don't itemize.

- The maximum deduction is $2,500 per year.

- The deduction is subject to income limitations.

- The loan must have been used for qualified education expenses.

- You'll need Form 1098-E to report the amount of interest you paid.

- The deduction can be claimed on Form

1040.

- Keep accurate records of all your student loan payments.

Remember these key points to maximize your tax savings.

Question and Answer

Q: Who is eligible for the student loan interest deduction?

A: You're eligible if you paid interest on a qualified student loan during the tax year, your modified adjusted gross income (MAGI) is below a certain threshold, and you're not claimed as a dependent on someone else's return.

Q: What is a qualified student loan?

A: A qualified student loan is a loan you took out to pay for qualified education expenses for yourself, your spouse, or a dependent. The loan must have been used to pay for tuition, fees, room and board, and other related expenses.

Q: How much can I deduct?

A: The maximum deduction is $2,500 per year. However, your actual deduction may be limited based on your income.

Q: Where do I claim the student loan interest deduction on my tax return?

A: You'll claim the deduction on line 33 of Form 1040.

Conclusion of Student Loan Interest Deduction: Maximize Your Tax Savings

The student loan interest deduction can be a valuable tool for reducing your tax liability and easing the burden of student loan debt. By understanding the eligibility requirements, deduction limits, and claiming process, you can maximize your tax savings and potentially free up some extra cash. Remember to keep accurate records of all your student loan payments and consult with a tax professional if you have any questions or complex situations. Take advantage of this tax benefit and start saving today!

Post a Comment