Debt Validation Letter Success Rate: What to Expect

Feeling overwhelmed by debt collectors and unsure if you even owe what they're claiming? You might have heard whispers of something called a "debt validation letter," a tool that can potentially challenge the legitimacy of a debt. But before you get your hopes sky-high, let's talk about what you can realistically expect in terms of success.

Dealing with debt collectors can feel like navigating a minefield. The constant calls, the confusing paperwork, and the sheer uncertainty of it all can leave you feeling stressed and powerless. You're likely wondering if there's a way to ensure these debt collectors are playing by the rules and if the debt they're pursuing is even valid in the first place.

So, what's the real deal with debt validation letter success rates? While there's no magic number guaranteeing your debt will disappear, sending a debt validation letter is a powerful tool. The success hinges on the debt collector's ability and willingness to provide the requested documentation. If they can't or won't, they may have to cease collection efforts. However, it's crucial to understand the process, timelines, and potential outcomes to set realistic expectations.

In essence, a debt validation letter is a formal request to a debt collector asking them to prove the debt is valid. Its success depends on the collector's response. A successful validation can force them to halt collections, but a failure to validate doesn't necessarily mean you owe the debt, just that they haven't proven it. Understanding the Fair Debt Collection Practices Act (FDCPA) is key, as it outlines your rights and the debt collector's responsibilities. Remember, this isn't a get-out-of-debt-free card, but a way to ensure fairness and accuracy in debt collection.

Understanding Factors Influencing Success Rate

This delves into the various elements that can affect how likely your debt validation letter is to achieve the desired result. It's not just about sending the letter; it's about the type of debt, the collector's practices, and your follow-up actions.

I remember a friend, Sarah, who was bombarded with calls about a medical bill she didn't recognize. She was understandably panicked. I suggested she send a debt validation letter, but she was skeptical, worried it was just a waste of time. She researched online and found conflicting information about success rates, which only added to her anxiety. The truth is, her success wasn't guaranteed, but sending the letter gave her control and provided valuable information.

Several things can influence the "success rate" of a debt validation letter. First, the age of the debt matters. Older debts are often harder for collectors to validate because records might be incomplete or missing. Second, the type of debt plays a role. Medical debt, for example, can be trickier to validate due to privacy regulations and complex billing processes. Third, the debt collector themselves impacts the outcome. Some companies are more diligent about record-keeping and compliance than others. A smaller, less sophisticated collection agency might be less likely to provide adequate validation than a large, established one.

Your actions also matter. Sending a well-crafted letter within the 30-day timeframe outlined by the FDCPA is crucial. Keeping detailed records of all communication with the debt collector is also essential. If the debt collector fails to validate the debt or continues to harass you after you've requested validation, you have options, including filing a complaint with the Consumer Financial Protection Bureau (CFPB) or even pursuing legal action. Ultimately, the "success rate" isn't just about whether the debt collector stops collection efforts; it's also about empowering you to understand your rights and navigate the debt collection process more effectively.

What Constitutes a Successful Debt Validation?

This section breaks down what a legally sound debt validation should look like. It clarifies the information a debt collector must provide to prove the debt is yours and valid.

A successful debt validation isn't just about the debt collector sending you something in the mail. It's about providing you with specific documentation that proves the debt is legitimate and that you are legally obligated to pay it. This documentation must be comprehensive and verifiable.

At a minimum, a valid debt validation should include the following: The name of the original creditor, the amount of the debt, the account number associated with the debt, a copy of the original contract or agreement that created the debt (such as a credit card agreement or loan document), and documentation showing that you are responsible for the debt (such as billing statements or account statements). The debt collector must also provide their name and address and state that they have the right to collect the debt.

It's important to scrutinize the validation documents carefully. Look for inconsistencies or inaccuracies. Does the account number match any accounts you've had? Does the name of the original creditor ring a bell? Are the dates and amounts correct? If anything seems off, don't hesitate to challenge the validation. A debt collector's failure to provide adequate validation doesn't automatically mean you don't owe the debt, but it does mean they may not be able to legally pursue collection efforts. In such cases, you may have grounds to request that they cease all contact with you regarding the debt.

The History and Myths of Debt Validation

This section explores the origins of debt validation rights and dispels common misconceptions surrounding the process. Many people harbor inaccurate beliefs about what debt validation can achieve, leading to unrealistic expectations.

The right to debt validation stems from the Fair Debt Collection Practices Act (FDCPA), a federal law enacted in 1977 to protect consumers from abusive debt collection practices. Before the FDCPA, debt collectors often engaged in harassing, deceptive, and unfair tactics to collect debts. The FDCPA sought to level the playing field by providing consumers with certain rights and protections, including the right to request validation of a debt.

One common myth is that sending a debt validation letter will automatically make the debt disappear. This is simply not true. A debt validation letter is a request for information, not a magic wand. If the debt collector can provide adequate validation, they are within their rights to continue collection efforts. Another myth is that debt validation only works for certain types of debt. While some debts may be more challenging to validate than others, the FDCPA applies to most types of consumer debt, including credit card debt, medical debt, and personal loans. A third myth is that you can only send a debt validation letter once. While you typically have 30 days from the initial communication to request validation under the FDCPA, you can still challenge the debt at any time if you have reason to believe it is inaccurate or invalid.

Understanding the history and dispelling these myths is crucial for setting realistic expectations and using debt validation effectively. It's a tool that can protect you from unfair or abusive debt collection practices, but it's not a guaranteed solution to debt problems.

Hidden Secrets of Debt Validation Success

This part reveals advanced strategies and techniques to maximize your chances of a favorable outcome when using debt validation. It goes beyond simply sending a standard letter and delves into the nuances of effective communication and documentation.

While a standard debt validation letter is a good starting point, there are hidden secrets that can significantly increase your chances of success. One secret is to be specific in your request. Don't just ask for "validation" of the debt; specify the exact documents you want to see, such as the original contract, account statements, and proof that you are the responsible party. The more specific you are, the harder it is for the debt collector to provide a generic or incomplete response.

Another secret is to use certified mail with return receipt requested. This provides proof that the debt collector received your letter and when they received it. This is crucial if you need to prove that you requested validation within the 30-day timeframe. A third secret is to keep meticulous records of all communication with the debt collector, including copies of all letters you send and receive, dates and times of phone calls, and the names of the people you spoke with. This documentation can be invaluable if you need to file a complaint with the CFPB or pursue legal action. Finally, don't be afraid to challenge the debt collector's response if you believe it is inadequate or inaccurate. If they provide documents that are incomplete, inconsistent, or illegible, send them another letter explaining why you believe their validation is insufficient and reiterate your request for specific documentation.

Mastering these hidden secrets can empower you to navigate the debt validation process more effectively and increase your chances of achieving a favorable outcome.

Recommendations for Improving Your Chances

This section provides practical advice and actionable steps you can take to improve your odds of a successful debt validation. It offers concrete tips on crafting effective letters, documenting communication, and understanding your rights.

Improving your chances of success with a debt validation letter involves a multi-faceted approach. First, carefully review the Fair Debt Collection Practices Act (FDCPA) to understand your rights and the debt collector's responsibilities. Familiarize yourself with the specific requirements for debt validation and the deadlines you need to meet.

Second, craft a clear and concise debt validation letter. Use a template as a starting point, but customize it to fit your specific situation. Be specific about the information you are requesting, and include a clear statement that you are requesting validation of the debt under the FDCPA. Third, document everything. Keep copies of all letters you send and receive, and record the dates and times of all phone calls with the debt collector. Note the names of the people you spoke with and summarize the content of the conversations. Fourth, be persistent. If the debt collector fails to provide adequate validation or continues to harass you after you've requested validation, don't give up. Send follow-up letters, file a complaint with the CFPB, and consider consulting with an attorney.

Finally, be realistic. Debt validation is not a guaranteed solution to debt problems. It's a tool that can help you ensure that you are only paying legitimate debts, but it's not a magic wand. If the debt collector can provide adequate validation, you may still be responsible for paying the debt. However, by following these recommendations, you can significantly improve your chances of achieving a favorable outcome and protecting yourself from unfair or abusive debt collection practices.

Debt Validation and Statute of Limitations

Debt Validation and Statute of Limitations intertwine in a nuanced way. Understanding the statute of limitations on debt can be a powerful tool in conjunction with debt validation. The statute of limitations is the time period within which a creditor can sue you to collect a debt. It varies by state and type of debt, typically ranging from three to six years.

Requesting debt validation doesn't automatically restart the statute of limitations, but acknowledging the debt or making a partial payment can. This is a crucial point to remember. Even if a debt collector can't validate a debt, they might still try to collect it if the statute of limitations hasn't expired. Therefore, it's essential to know the statute of limitations in your state for the specific type of debt you're dealing with.

If the statute of limitations has expired, the debt is considered "time-barred," meaning the creditor can no longer sue you to collect it. However, they can still try to collect the debt voluntarily. You can send them a cease and desist letter, demanding they stop contacting you about the debt. Be cautious about acknowledging a time-barred debt, as this could potentially revive it in some states. Debt validation and the statute of limitations are separate but related concepts. Debt validation is about verifying the legitimacy of the debt, while the statute of limitations is about the time period within which a lawsuit can be filed. Understanding both can empower you to effectively manage your debt and protect your rights.

Tips for Writing an Effective Debt Validation Letter

Creating a strong, well-structured letter is essential. This section offers concrete advice on the language to use, the information to include, and the overall tone to adopt to maximize the impact of your request.

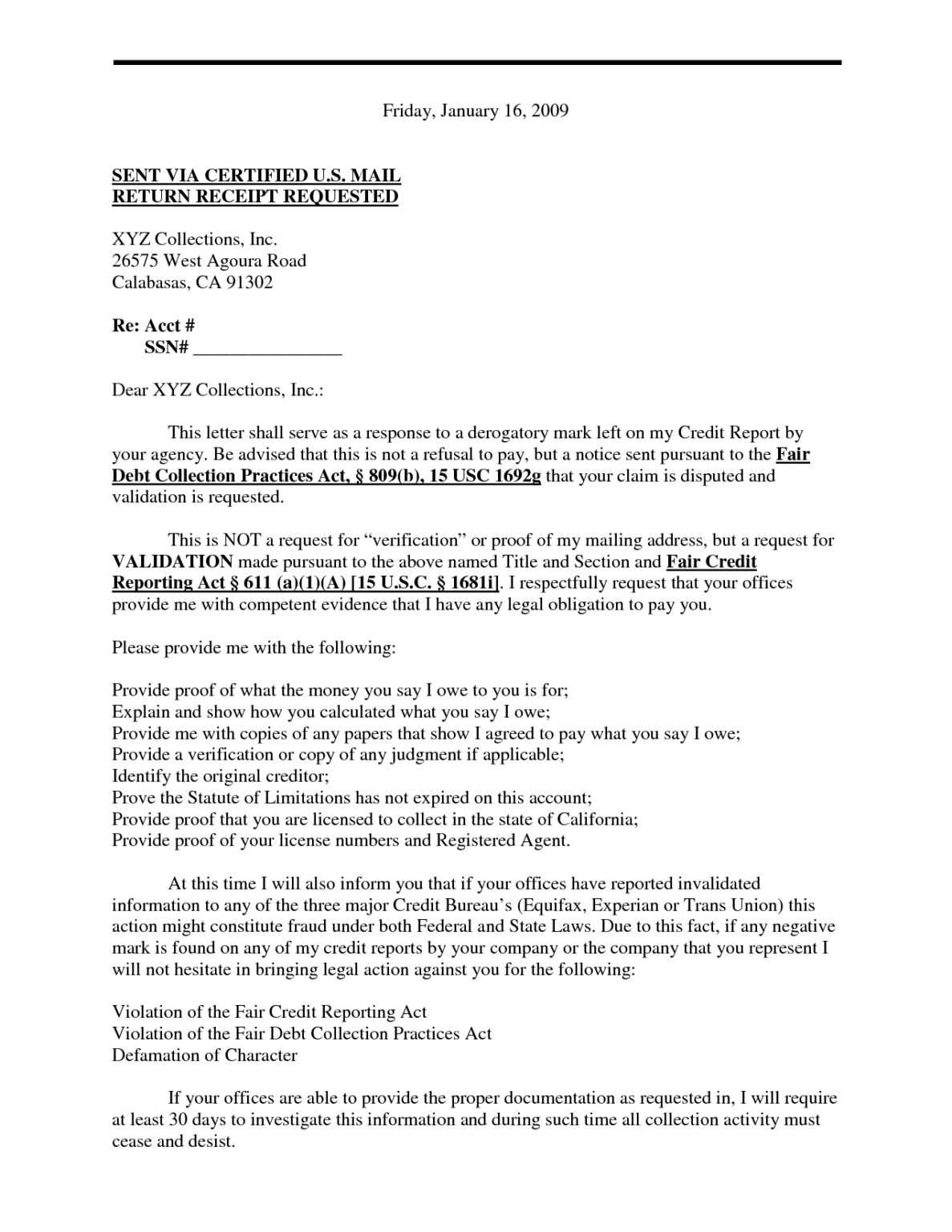

Writing an effective debt validation letter is crucial for getting the information you need and protecting your rights. First, start with a professional and polite tone. While you may be frustrated or angry, it's important to remain respectful and avoid using accusatory language. Second, clearly state that you are requesting validation of the debt under the Fair Debt Collection Practices Act (FDCPA).

Third, be specific about the information you are requesting. Ask for copies of the original contract, account statements, and any other documents that support the debt collector's claim. Fourth, include your name, address, and account number (if known). This will help the debt collector identify your account and respond to your request. Fifth, set a clear deadline for the debt collector to respond. Under the FDCPA, they have 30 days to provide validation of the debt. Sixth, send your letter via certified mail with return receipt requested. This will provide proof that the debt collector received your letter and when they received it. Finally, keep a copy of your letter for your records.

In addition to these general tips, there are a few specific things to avoid. Don't admit that you owe the debt, even if you think you do. Don't offer to make any payments, even small ones. Don't provide any personal information that the debt collector doesn't already have. By following these tips, you can write an effective debt validation letter that will help you protect your rights and ensure that you are only paying legitimate debts.

Common Mistakes to Avoid When Sending a Debt Validation Letter

Navigating the debt validation process can be tricky, and it's easy to make errors that could weaken your position. This section highlights the most frequent pitfalls to watch out for and how to avoid them.

When sending a debt validation letter, avoiding common mistakes is as important as crafting a good letter. One of the biggest mistakes is waiting too long to send the letter. Under the FDCPA, you only have 30 days from the initial communication from the debt collector to request validation. If you wait longer than 30 days, you may lose your right to demand validation.

Another common mistake is failing to send the letter via certified mail with return receipt requested. This provides proof that the debt collector received your letter, which can be crucial if they later claim they never received it. A third mistake is admitting that you owe the debt in your letter. Even if you think you do owe the debt, avoid making any statements that could be construed as an admission of liability. A fourth mistake is not being specific about the information you are requesting. Don't just ask for "validation" of the debt; specify the exact documents you want to see. A fifth mistake is not keeping a copy of your letter and any documents you receive from the debt collector. These records can be invaluable if you need to file a complaint or pursue legal action. Finally, don't ignore the debt collector's response. If they provide validation documents, carefully review them to ensure they are accurate and complete. If you believe the validation is inadequate, send them another letter explaining why.

By avoiding these common mistakes, you can significantly increase your chances of success with debt validation.

Fun Facts About Debt Validation

Lighten the mood with some interesting and lesser-known facts about debt validation. This can make the topic more engaging and memorable.

Debt validation isn't always a dry, legalistic process. Here are a few fun facts that might surprise you. Did you know that debt collectors are required to cease collection efforts if they cannot validate a debt within 30 days of receiving your request? That's a powerful incentive for them to provide accurate and complete information. Also, some debt collectors may actually buy debts for pennies on the dollar. This means they could be trying to collect a debt that they acquired for a fraction of its original value.

Another interesting fact is that the Fair Debt Collection Practices Act (FDCPA) not only protects consumers from abusive debt collection practices but also requires debt collectors to disclose certain information about the debt, such as the name of the original creditor and the amount of the debt. Debt validation has been around since 1977 when the FDCPA was enacted, but many consumers are still unaware of their right to request validation of a debt. Finally, while debt validation can be a powerful tool for protecting your rights, it's not a substitute for managing your debt responsibly. The best way to avoid debt collection problems is to pay your bills on time and avoid accumulating excessive debt in the first place.

These fun facts highlight the importance of understanding your rights and taking proactive steps to manage your debt effectively.

How to Write a Debt Validation Letter

A step-by-step guide to crafting a compelling and legally sound debt validation letter. This section provides a template, examples of effective language, and tips for formatting.

Writing a debt validation letter can seem daunting, but it's a straightforward process with a few key steps. First, find a template online. Numerous websites offer free debt validation letter templates. Choose one that is clear, concise, and complies with the Fair Debt Collection Practices Act (FDCPA).

Second, customize the template to fit your specific situation. Include your name, address, and account number (if known). Clearly state that you are requesting validation of the debt under the FDCPA. Specify the information you are requesting, such as copies of the original contract, account statements, and proof that you are the responsible party. Set a clear deadline for the debt collector to respond, typically 30 days. Third, proofread your letter carefully for any errors or omissions. Ensure that all information is accurate and complete. Fourth, print your letter and sign it. Fifth, send your letter via certified mail with return receipt requested. This will provide proof that the debt collector received your letter and when they received it. Sixth, keep a copy of your letter and the return receipt for your records.

In addition to these steps, there are a few general tips to keep in mind. Use a professional and polite tone. Avoid admitting that you owe the debt. Don't offer to make any payments. Don't provide any personal information that the debt collector doesn't already have. By following these steps and tips, you can write an effective debt validation letter that will help you protect your rights.

What If the Debt Collector Validates the Debt?

This section addresses the scenario where the debt collector provides adequate validation. It outlines your options if you still believe the debt is inaccurate or unfair.

If the debt collector successfully validates the debt, it means they have provided sufficient documentation to prove that the debt is legitimate and that you are legally obligated to pay it. However, this doesn't necessarily mean that you have no further recourse. You still have options if you believe the debt is inaccurate or unfair.

First, carefully review the validation documents. Look for any errors or inconsistencies. If you find any mistakes, send the debt collector a letter disputing the debt and explaining why you believe it is inaccurate. Second, request verification of the debt. Verification is a more detailed investigation than validation. It requires the debt collector to provide additional documentation, such as payment records and a detailed breakdown of the debt. Third, consider negotiating a settlement with the debt collector. They may be willing to accept a lower amount than the full balance owed. Fourth, if the debt is valid but you cannot afford to pay it, explore options such as debt management plans, debt consolidation loans, or bankruptcy. Finally, if the debt collector continues to harass you after you have requested validation or verification, file a complaint with the Consumer Financial Protection Bureau (CFPB) or consider consulting with an attorney.

While a successful validation means the debt collector has met their legal obligation, it doesn't mean you have to simply give up. By taking these steps, you can continue to protect your rights and explore all available options.

Listicle: 5 Things to Know About Debt Validation Success

A concise summary of the most crucial points in a list format, making the information easily digestible and shareable.

Debt validation can be a powerful tool, but it's essential to understand the key factors that influence its success. Here are 5 things you need to know: 1. Understand Your Rights: The Fair Debt Collection Practices Act (FDCPA) gives you the right to request validation of a debt. Know your rights and use them.

2. Act Quickly: You only have 30 days from the initial communication from the debt collector to request validation. Don't wait, send your letter promptly.

3. Be Specific: Clearly state what information you are requesting, such as copies of the original contract and account statements. The more specific you are, the better.

4. Document Everything: Keep copies of all letters you send and receive, and record the dates and times of all phone calls. This documentation can be invaluable.

5. Don't Give Up: If the debt collector fails to provide adequate validation or continues to harass you, don't give up. File a complaint with the CFPB and consider consulting with an attorney.

By keeping these 5 things in mind, you can significantly increase your chances of success with debt validation and protect yourself from unfair or abusive debt collection practices.

Question and Answer

Q: What happens if a debt collector doesn't respond to my debt validation letter?

A: If a debt collector fails to respond to your debt validation letter within 30 days, they are required to cease collection efforts. This means they cannot contact you, file a lawsuit against you, or report the debt to credit bureaus until they provide validation.

Q: Does debt validation affect my credit score?

A: Requesting debt validation itself does not directly affect your credit score. However, if the debt is reported to credit bureaus and you don't address it, it could negatively impact your score. Debt validation can help you ensure that only accurate and valid debts are reported on your credit report.

Q: Can I still request debt validation if I already made payments on the debt?

A: Yes, you can still request debt validation even if you have already made payments on the debt. Making payments doesn't waive your right to request validation and ensure the debt is legitimate.

Q: What if the debt collector sends me a bunch of legal jargon that I don't understand?

A: If the debt collector sends you documents that are confusing or filled with legal jargon, don't hesitate to ask them to explain it in plain language. You can also consult with a consumer law attorney or a non-profit credit counseling agency for assistance.

Conclusion of Debt Validation Letter Success Rate

Debt validation is a valuable consumer right, but understanding its limitations and potential outcomes is key. While it isn't a guaranteed debt eraser, it's a powerful tool for ensuring fairness and accuracy in debt collection. By understanding the factors influencing success, crafting effective letters, and knowing your rights, you can navigate the debt collection process with confidence and protect yourself from unscrupulous practices.

Post a Comment